|

|||||||||||||||||

|

Inflation Surge Is No Need For Hysteria

General Gemma Riley-Laurin 17 Nov

General Gemma Riley-Laurin 17 Nov

|

|||||||||||||||||

|

General Gemma Riley-Laurin 15 Nov

|

|||||||||||||||||||||||

|

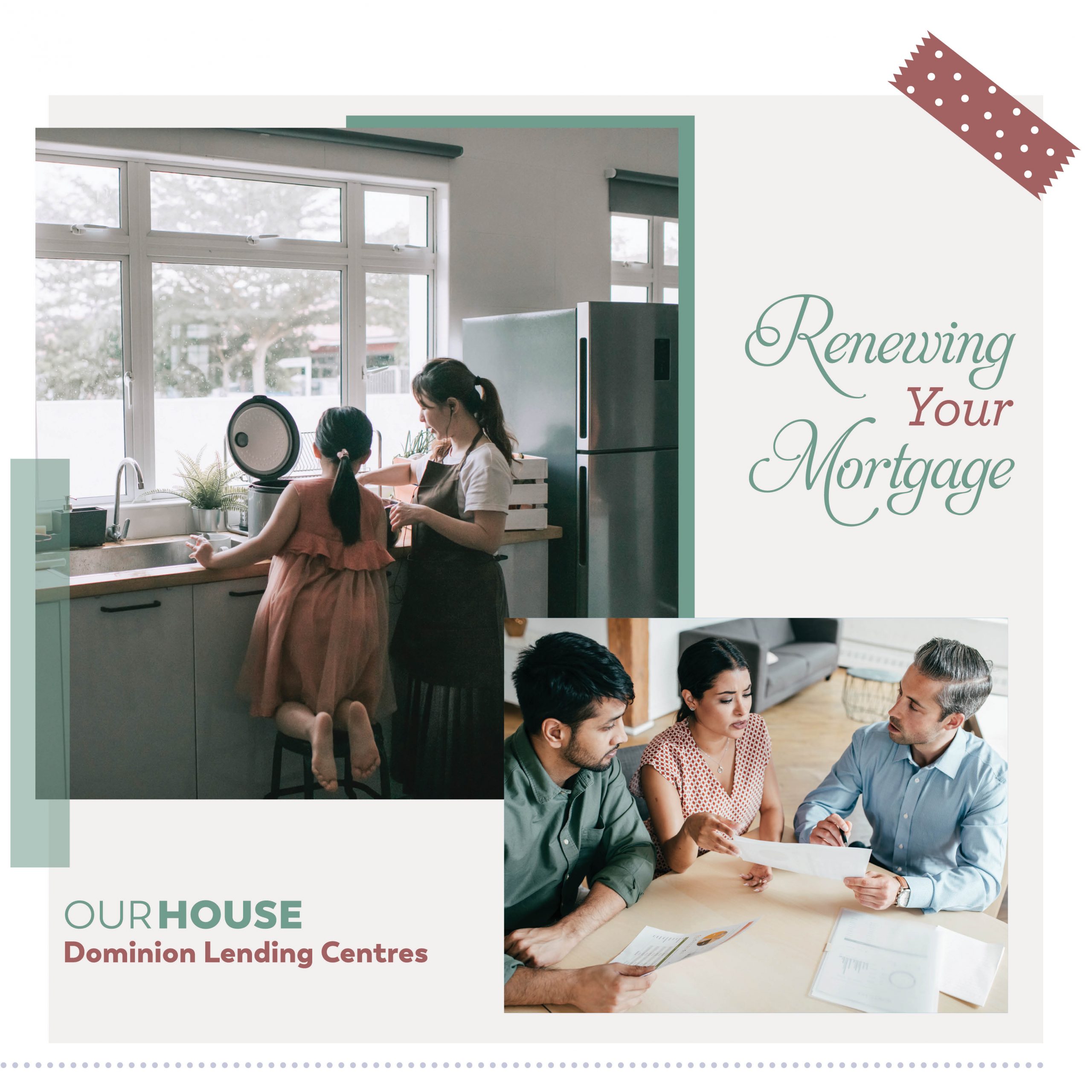

General Gemma Riley-Laurin 12 Nov

Did you know? Close to 70 percent of mortgages never make it to the end of their term! This means that, for a variety of reasons, homeowners are ending their mortgages early. However, that still leaves a solid 30 percent of home buyers who keep their mortgage until the term is up and it is time to renew!

If you are not planning to move in the near future and are happy with your current mortgage, you are likely one of the 30 percent who will renew once the term ends. So what does this process look like?

When it comes time to renew your mortgage, most lenders will send you a renewal letter when there is around 3 months remaining on your term. While nearly 60 percent of borrowers simply sign and send back their renewal without ever shopping around for a more favourable interest rate, this is actually the best time to check out your options.

Most standard terms are 5-year terms and, with that much time having passed since signing, the market rates could be very different once the term is up! Despite this, lenders tend to provide higher rates on renewals versus new clients as they are hoping that the ease of renewal will prevent you from seeking out new rates. However, shopping around for a better rate is not as difficult as it sounds – especially with the help of a mortgage broker – and it could end up saving you a couple hundred dollars a month (depending on your situation)! Ideally, you should be keeping track of your own mortgage term end date as shopping for a new rate between four and six months before your expiry will ensure you are able to find the most affordable option for you.

After shopping around, you may find that your bank is actually offering a great rate – in which case you can simply submit the renewal! But if you are able to seek out a lower rate, we promise you will thank yourself for putting in the effort to find out! As another point of interest, renewal time is also a great time to make an extra payment on your mortgage, if you are able!

Beyond renewing your mortgage, home owners also have the option to transfer or switch the mortgage. This can be done any time during the term of the mortgage but may have penalties associated with breaking the mortgage before the term is up. Transfering to another lender is generally done to get a better rate, but you will need to go through the entire mortgage process again – including the ‘stress test’ – which makes shopping around at renewal time an even smarter option.

If your mortgage is coming up for renewal and you want to find out what lower rates may await you, contact your local mortgage professional! They can help you find the best option for where you are at in your life now and help you to ensure future financial success.

General Gemma Riley-Laurin 5 Nov

|

|||||||||||||||||||

|

|||||||||||||||||||

|